“The test of a first-rate intelligence is the ability to hold two opposed ideas in mind at the same time and still retain the ability to function.”

SCOTT FITZGERALD “THE CRACK UP” (1936)

The current market environment, maybe more than ever, demands this Fitzgeraldian test of the portfolio manager. For example, how do you build a portfolio that acknowledges, at once, the near-decade sustained bullish trend of equity markets and also valuation levels unrivaled by any point in history except levels prior to the Great Depression and the Dot-Com Bust of the early 2000s? For the trend-follower or momentum trader, the answer is easy: buy stocks. For the valuation-driven or macro investor, the answer is easy: sell stocks. At Martello, we account for this inherent tension between valuation and trend when building portfolios. As an aside, we utilize two different methods to take both the valuation and technical into account: valuation-based overlays and strategy ensembling. These might sound complicated, but in fact are quite straightforward and we believe the sensical way to tackle this issue. In both cases, what this means is that we give weight to both the value and technical factors. When valuations are cheap and the trend is bullish, we load up our exposure. When the picture is less clear, we reduce our exposure to more modest levels. When all signs are bearish, we can throttle down all the way.

In addition to equity market valuation, we continue to see competing signals in different segments of the fixed income market. Any regular reader of our monthly notes knows that we have been harping on the rising risk of traditional fixed income approaches given the prospects of rising inflation in the US, low real interest rates, and the Fed’s expectation of additional rate hikes in the coming months. In the corporate world, years of utilizing cheap debt financing to buy back shares has left companies significantly more levered. As a side-note, research has shown that corporations generally have a bad record of timing corporate buybacks. Most tend to do it to further drive equity prices higher (and it makes sense to buy back rather than increase dividends from the investor’s point of view) but these buybacks often occur near the top of a cycle.

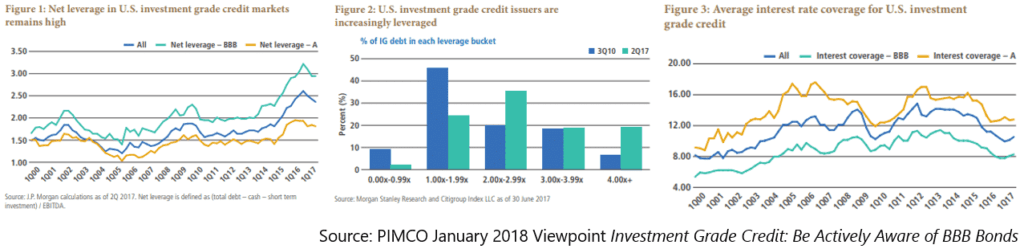

Even in investment grade credit, to quote the famed market philosopher Yogi Berra, “the future ain’t what it used to be.” A recent paper by PIMCO showed that A and BBB-rated credit, the lower end of the investment grade universe, have more than 50% higher leverage today than before the Great Financial Crisis (Figure 1 below) and the investment grade universe is comprised of higher-leverage borrowers (Figure 2). At the same time, interest coverage ratios for this universe (a ratio showing how much money a company makes compared to its interest expense on debt) has fallen to levels near or below the depths of the financial crisis (Figure 3). Think about that for a second; by this metric, the credit quality of these companies is near the same levels as at the bottom of the worst recession since the Great Depression, despite all the economic progress over the last decade. In fact, interest coverage ratios for these companies have been FALLING for years despite steady economic growth, record corporate profits, and historically wide profit margins.

On one hand, you can understand the rationale for companies to do this; levering up when debt is cheap is Corporate Finance 101. If the cost of debt is less than the cost for issuing equity, borrowing makes more sense than issuing stock. The problem with debt financing, however, is that it creates additional inflexibility when things take a turn for the worse; you can reduce or suspend the dividend to your equity holders, but that is not an option when the bondman cometh for his coupon. The likely result of a significant recession, which would almost certainly further impair companies’ ability to service debt, would be what’s known as a “ratings migration.” A ratings migration in this context simply means a lot of companies would be re-rated to lower credit qualities to more appropriately reflect their financial position and leverage levels, and therefore higher rates on debt to reflect this increased credit risk. Depending on how quickly that happens, this could cause significant forced selling pressure from index-based strategies that would be forced to sell if a bond falls below the mandated universe of credit quality.

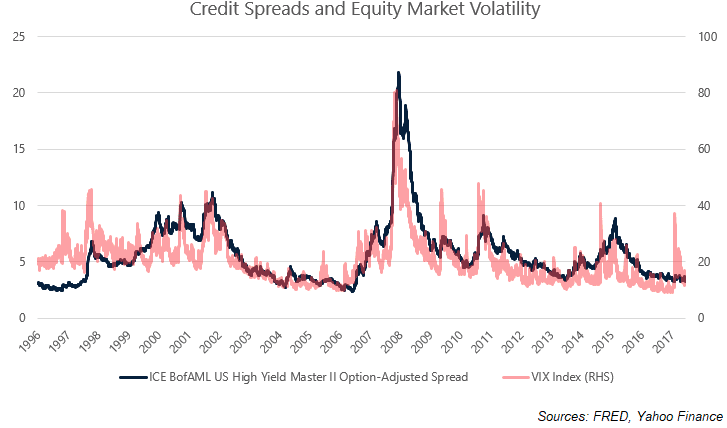

There are deeper implications for investors here, not only in credit markets but also for stocks. As the chart below shows, equity market volatility and credit spreads are very tightly linked. This isn’t a coincidental phenomenon; if a stock is a claim on a company’s future profits, it would make sense that stocks would become more volatile in times of when debt is more expensive, because more expensive debt obviously imperils a company’s profitability.

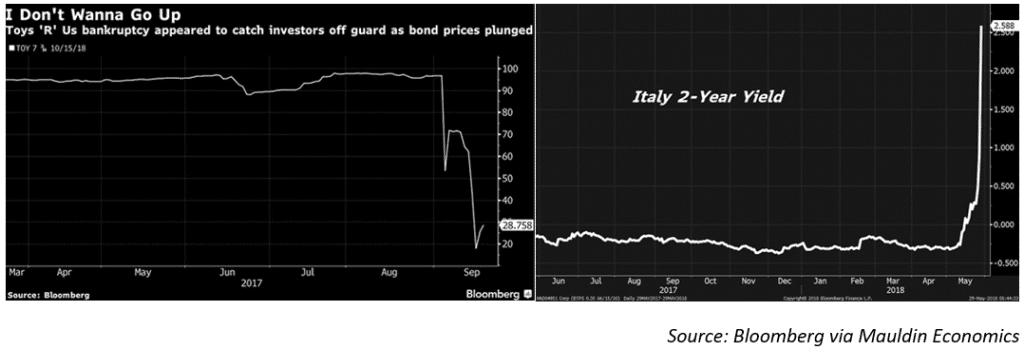

While the additional leverage and deteriorating credit quality is concerning on its own, we also see signs of structural weakness that increases shock risk in fixed income markets. One of these signs is the seemingly disorderly reaction of markets to negative events. Jared Dillian of Mauldin Economics covered this in his recent piece “Wall Street Fired Too Many People,” highlighting the price response to the Toys R Us bankruptcy announcement and the recent spike in Italian bond yields after the election. In both cases, which Dillian calls an “instantaneous blowup in the capital markets,” he highlights that these risks should be priced in over time, and the fact that they weren’t shows structural problems in the market. The Toys R Us bankruptcy, for example, should not have caught investors off guard, as credit analysts should have seen deteriorating financials for quarters or years, and this bankruptcy risk would have been slowly priced over time. There are likely several reasons for these structural failings, including the reduction in market making activity in more opaque markets such as bonds; dealer inventory in these securities has plummeted in the years since the crisis due to regulatory factors. Once again, the impact of the passive investing revolution is also at work here; with more and more assets linked to index-based products or quasi-indexed strategies, research on individual securities has been devalued in favor of buying/selling a whole basket.

Back to Fitzgerald’s quote, it is important to remember that this is just one side of two opposing views. Despite our perception of increasing risk in fixed income, some of our models continue to utilize various government and corporate bond ETFs for a variety of reasons including diversification benefit and income potential. As we mentioned above, we build our models by incorporating many factors in combination. However, given the structural issues mentioned above, as well as seemingly deteriorating fundamentals and a poor macro picture for bonds (rising rates, increasing inflation, etc.), investors must be increasingly aware of the hidden risks in their bond portfolios.

We thank our readers, as always, for your time and interest. As of this month, we have stopped generating the usual second half of our monthly write-up, which summarized the previous month’s market returns and recent events. If you would still like to receive this information monthly, please feel free to let us know and we may include it again in the future.

Sincerely,

Arthur Grizzle & Charles Culver

Managing Partners

Martello Investments