Hurricanes: The last several weeks has seen major Hurricanes Harvey and Irma bring incredible destruction to the people of Texas, Florida, and the Caribbean. In the aftermath of these catastrophes, it seems that Wall Street and the investment community at large is obsessed with prognosticating the ultimate impact of the storms on economic growth and the stock market. Not only do we find this type of analysis objectionable in the face of much personal disaster, we find the economic arguments on both sides of the debate lacking; in addition, historical data shows that the analysis is useless regarding the stock market.

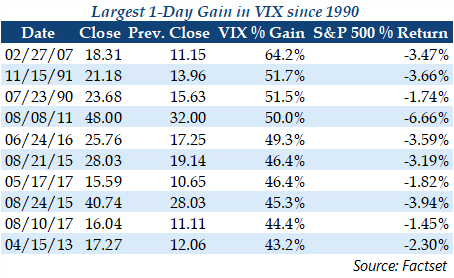

August Market Recap: Equity markets were mixed in August, with the S&P 500 posting a modest 0.3% gain. Emerging Markets and the Technology sector were leaders for the month, while Energy stocks and small cap lagged. The market also endured two significant VIX spikes in August, including the 9th largest one-day percentage move in the VIX since 1990. Fixed income market indices generally rallied, though high yield credit spread expanded on bearish reports from several banks and investment managers. Expectations for damage to Texas refineries sent oil prices lower and gas prices higher. The US Dollar continued to fall, and is down 9.3% year-to-date.

As surely all of you know, this season has thus far brought two major hurricanes to the US. The first, Harvey, made landfall in southern Texas as a Category 4 and is widely considered to be the wettest Atlantic hurricane on record. The second, Irma, hit the Florida Keys as a Category 4 in mid-September, turning northward and raking the entire state of Florida. As of the time of this writing, the combined death toll from Harvey and Irma approached 100, and residents of Texas and Florida are assessing the damage before beginning the lengthy process of rebuilding. Still, typical for these types of disasters, the days following the hurricanes saw a barrage of reports from big banks and investment companies discussing the potential impact of the storms on the economy and the stock market. These reports are filled with statistics about the size of the Houston economy (fourth largest in the US) and estimates for how much the storm might drag down GDP in the short-term or, even worse, how natural disasters are a boon to the economy because of the stimulative impact of increased spending during the recovery period. These are the same clowns that argue that war is good for the economy because of increased defense spending (never mind the death and destruction). Putting aside the actual economic argument of the hurricanes for now, this is the type of cold, detached analysis that causes people to despise Wall Street and the investment industry in general. A line from the fictional Ben Rickert in the movie The Big Short rings true here:

“You know what I hate about…banking? It reduces people to numbers. Here's a number - every 1% unemployment goes up, 40,000 people die, did you know that?”

This is more personal for me than most; I grew up in the Florida Keys, where dealing with hurricanes is an annual ritual, and where Hurricane Irma made landfall last weekend. I appreciate the good wishes I received from many of you over the last week. My family was fortunate this time, as everyone is safe and property damage was minimal. Others were not so lucky, particularly the Middle and Upper Keys not to mention the people of the worse-hit Caribbean islands. In the wake of these events, I wish analysts on Wall Street and the financial advisory community could show some restraint. I would be willing to bet that not a single person in Texas or Florida that has lost a loved one, a home, or a business due to Harvey or Irma cares about the impact of the storm on GDP growth and the stock market.

There are many reasons to not trust disaster-focused economic or market analyses, not the least of which is that the theories underpinning them are debatable at best, and more likely unknowable. The arguments on both sides are clear. The “pro-natural disaster for growth” camp argues that the economy will receive a short-term boost caused by the stimulative impact of increased spending as communities rebuild and, funded by insurance payouts, the injection of funds into the real economy will increase the velocity of money, further improving economic growth and boosting inflation. The “anti-natural disaster for growth” camp points out that increased spending caused by hurricane recovery efforts, while providing a short-term boost to growth, is just robbing future spending and growth, washing out the overall impact (pun not intended). In addition, the reduction in income and discretionary consumption at least partially offsets the “positive” impact of recovery-related spending. As I said, these theories are debatable at best and ultimately matter little; economies are highly complex adaptive systems, making it essentially impossible to evaluate the impact of any specific underlying factor at any specific point in time.

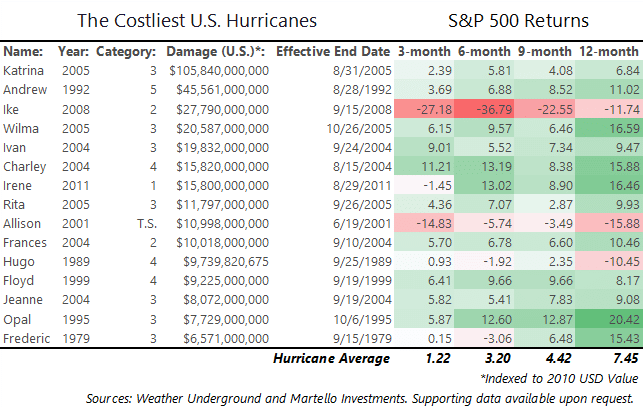

Not only that, but regarding the stock market, the analysis is, in fact, completely useless. The truth is that the costliness of hurricane damage and its estimated impact on GDP (either positive or negative) have zero effect on the market. Below find a table of the costliest US hurricanes since 1979 and the returns of the S&P 500 in the months following the end of the storm. The most glaring conclusion to draw from this data is that the market, on average, delivers returns roughly in line with historical averages following the landfall of an extremely destructive hurricane.

The point, however, is not to search for meaning in the movements of the stock market following a natural disaster; it is, in fact, to do the exact opposite. There is much to be done in the aftermath of such catastrophes. The destruction in Texas from Harvey is saddening, and early reports from the Keys are grim. FEMA estimates that a quarter of the homes in the Keys are destroyed, and full recovery will likely take months, if not years. I know several organizational efforts underway throughout the state to collect, ship, and distribute supplies to people in need in the Keys. I will participate in these, and am happy to pass on information for others looking to help as well.

-A.G.

Domestic stock indices were mixed in August, and this year’s trend of large cap stocks outperforming small cap continued. US Large Cap stocks, as measured by the S&P 500 Index, gained 0.3% for the month, while the Russell 2000 small-cap index returned -1.3%. Year to date, the S&P 500 has gained 11.9% compared to a 4.4% gain for the Russell 2000; on a rolling 8-month basis, small cap is underperforming at the worst rate since April 2016, when the market was rebounding from correction levels. International developed stocks were flat, while Emerging Markets, as measured by the MSCI Emerging Markets Index, rallied 2.3% for the month to bring year-to-date gains to 28.6%. At the sector level, Technology stocks led the market with a 3.5% gain, bringing year-to-date gains to 26.6%. Energy lagged the market with a -5.2% return, as a weak oil market continues to weight on the sector. Market volatility, as measured by the CBOE Market Volatility Index (VIX) finished the month only slightly higher, closing August at 10.59 after closing July at 10.26. The market, however, endured two significant volatility spikes intra-month, a 44% spike on August 10th and a 32% spike on August 17th. The August 10th spike was the 9th largest in the VIX on record, which is significant given the equity market’s return for the day (-1.45%) was relatively benign compared to returns in similarly dramatic VIX spikes.

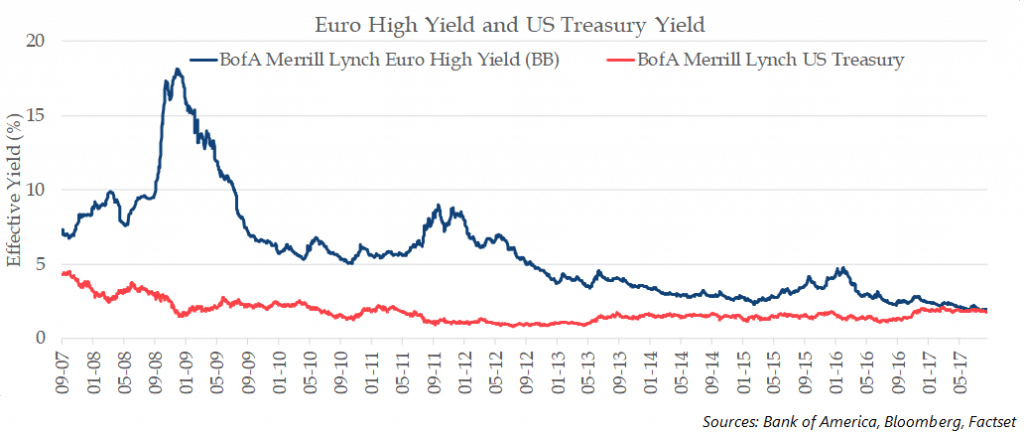

Fixed Income markets delivered solid returns in August, with the Bloomberg Barclays US Aggregate Index rallying 0.9% for the month. The US Treasury yield curve flattened in August, with the 2-year Treasury yield falling 4 bps to 1.32%, the 10-year Treasury yield declining 17 bps to 2.12%, and the 30-year Treasury yield falling 17 bps to 2.72%. High yield credit spreads, as measured by the BofA Merrill Lynch US High Yield Option-Adjusted Spread, rose 24 bps off of historically low levels to close August at 3.85%. High yield spreads were impacted by bearish reports from several large banks and investment managers citing significant compression in yield on low credit-quality companies. Recently, Bank of America highlighted European High Yield bonds in particular, which now trade at similar yields to US Treasury bonds.

The S&P GSCI Total Return Index returned -0.8% in August, as falling prices of oil and agricultural commodities weighed on the index for the month. Hurricane Harvey significantly impacted the energy market in August, as the anticipated damage to refineries in Texas caused refined products to rally, with Gasoline [+12.7%], Heating Oil [+4.4%], and Gasoil [+3.2%], each posting gains on the month. At the same time, Crude Oil prices fell for the month, as damage to refineries could impact demand for oil in the short-term. West Texas Intermediate (WTI) Crude Oil opened the month at $50.17/bbl. and traded down through August to close the month at $47.09/bbl. Agricultural commodities Soybeans [-6.1%], Corn [-7.0%] and Wheat [-13.3%] fell sharply following a report by the US Department of Agriculture (USDA), which forecasted supply higher than expectations. Geopolitical tension and uncertainty about the timing of Fed tightening was a tailwind for Gold and Silver, which posted monthly gains of 3.9% and 4.3%, respectively.

The US Dollar continued to weaken in August, with the US Dollar Index falling 0.2% in August. The Index, which measures the US Dollar’s value against a basket of 6 foreign currencies, is now down 9.3% year-to-date, as expectations of spending cuts by the new Republican regime have faded and investors question the pace of tightening by the Fed.

The US Dollar continued to weaken in August, with the US Dollar Index falling 0.2% in August. The Index, which measures the US Dollar’s value against a basket of 6 foreign currencies, is now down 9.3% year-to-date, as expectations of spending cuts by the new Republican regime have faded and investors question the pace of tightening by the Fed.

Sincerely,

Arthur Grizzle & Charles Culver

Managing Partners

Martello Investments