Valuation: The strong bull rally over the last 8 years continues to expose the inherent tension between valuation metrics flashing warning signs and technical or sentiment-driven factors leading the market higher. Though valuation is not a tradeable signal over the short-term, we acknowledge its important role in portfolio construction and risk analysis. This month, we delve into the Cyclically-Adjusted Price to Earnings Ratio (CAPE), analyzing its historical significance in forecasting long-term equity market returns, and what the current ratio value may tell us about the level of risk in the market and the opportunity set moving forward.

Markets: The equity markets capped off a strong first-half of the year with a solid return in June, though increased hawkishness from Fed and ECB officials caused a slight sell-off in the last two weeks of the month. Technology stocks, leading the market so far in 2017, sold off sharply in June, and volatility markets are showing a tick-up in investor fear regarding the tech sector. Central bankers’ comments were more impactful in the bond market, particularly in short-duration US Treasuries and across the curve in developed Europe, where yields rose significantly. Commodity prices continue to fall, weighed down by a weak oil market.

I have a friend, whom we will call Jeff, who was (and still is) responsible for running a large family trust at the start of the millennium. It was certainly a different time back then. Stock markets were on an incredible run, screaming to all-time highs as valuations reached record levels. Unproven, unprofitable companies were going public. The idea that technology could change life as we know it was infectious, so much so, in fact, that it caused investors to incorporate new valuation techniques into market lexicon, casting aside mundane metrics such as profit and sales for “eyeball count” and “page visits.” Though the internet would certainly change life as we know it, many failures were left along the way, and the ultimate market crash left many investors’ capital permanently impaired. Jeff never saw it coming. He had invested so much in so many hyped technology stocks and, like so many others, nearly lost everything ignoring the warning signs in search of the next big thing.

It’s been a great market for stocks since the last financial crisis ended. Stock markets have made a string of all-time highs recently while valuations rise toward bubble levels, though not as lofty as during the height of the dot-com bubble. Technology is leading the market higher and investors have once again lost their taste for earnings and cash flow, instead favoring growth over profits, adjusted accounting metrics, and Fed-watching. The market’s resilience over the last few years is certainly astounding, particularly in the midst of continued dysfunction from Washington and increasing geopolitical tension across the world. At the same time, the elevated valuation over the last several years has stirred the perma-bears, those with the singular message that the overvalued market is primed for an imminent crash, from hibernation.

As we have highlighted in previous letters, bubbles and market tops are best spotted with the benefit of hindsight, and valuation is not a catalyst in and of itself. Still, we acknowledge that market valuation has an important role to play in risk analysis and portfolio construction. So, this month we want to explore the current valuations we see today, and what that may tell us about the opportunity set for the coming years.

An extremely bullish equity market exposes the inherent tension between trend/momentum trading and macroeconomic/valuation-driven investing. The recent bull run in the equity market over the past 8 years since the crisis trough in 2009 has been characterized as the most hated bull market ever, in part because the market has remained at elevated valuation levels compared to historical norms for a considerable length of time. Trend-following, valuation-agnostic by definition, is generally used for short-to-intermediate-term market analysis because valuation metrics are generally only useful over long time periods. Though under- or over-valuation may not be a tradeable signal, it can be useful to frame the level of market risk and strategically tilt asset class exposure.

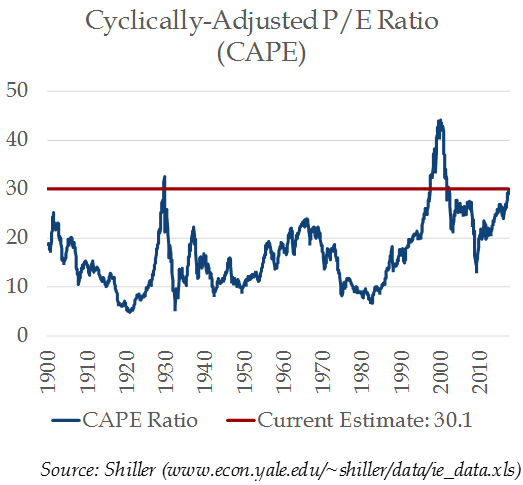

There are many worthy long-term valuation metrics, but for the purposes of this commentary we will focus on the Cyclically-Adjusted Price to Earnings Ratio (CAPE), made famous by economist Robert Shiller in his book Irrational Exuberance. The CAPE ratio is a version of Price/Earnings which uses 10-year average inflation-adjusted earnings to smooth out the impact of cyclical earnings noise. The CAPE ratio has received a lot of press lately, most of which focuses on the level of the ratio relative to historical peaks. The current value (approximately 30) is higher than pre-crisis levels in 2007, and is surpassed only by valuations seen prior to the dot-com bust and the pre-Great Depression levels of the late 1920s.

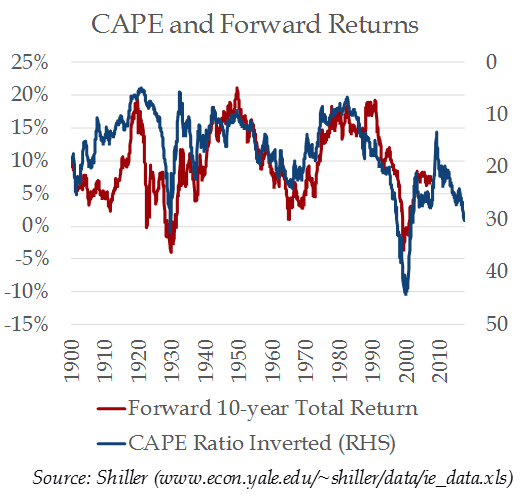

Visually comparing the CAPE ratio to long-term equity returns shows that the valuation metric has some power at least directionally: high valuation generally leads to lower forward returns, while low valuation generally leads to higher forward returns.

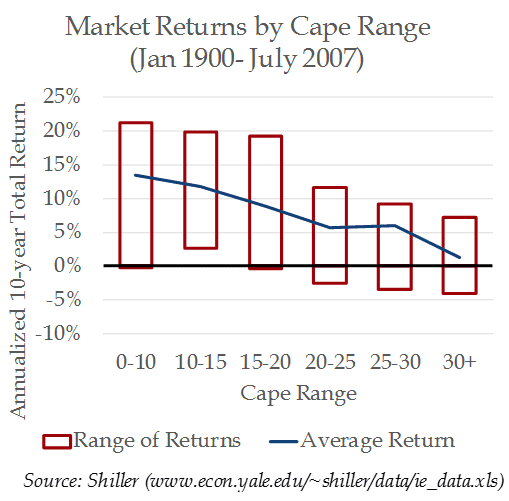

Analyzing CAPE in ranges shows the impact of valuation on risk; lower CAPE valuation ranges tend to de-risk the portfolio in terms of worst observed outcome while higher valuation ranges have more negative worst outcomes. To be clear, these charts show CAPE against 10-year annualized forward returns for the equity market; the current CAPE ratio value (approximately 30) is historically followed by very low long-term returns, even negative in some cases. A 10-year annualized return near or below zero is obviously catastrophic for an investor’s ability to generate wealth.

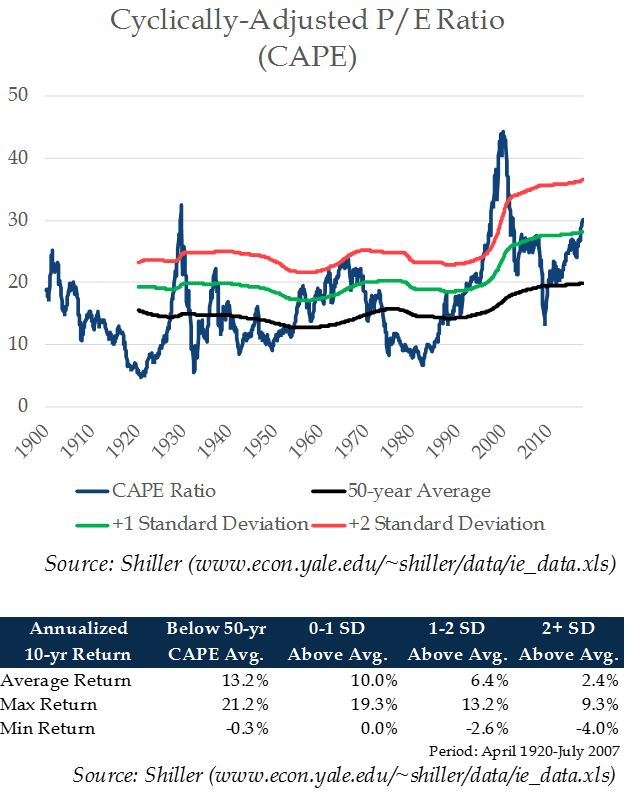

A notable criticism of long-term ratio analysis is the idea that the market environment is different, meaning that it is not appropriate to compare current equity market valuations to valuations of the past for one reason or another. A common argument cites changes in economic development; the US now, as a leading global economy, certainly justifies a higher valuation compared to the early 1900s when the country was still an emerging market. To accommodate these criticisms in our analysis, we compared CAPE to a 50-year average (45-60 years is sometimes thought of as a super-cycle), which should account for long-term cyclical factors. Once again, it is clear that the average return to investors improves with lower CAPE valuations, but also that the worst observed outcome (Min Return) is more favorable in lower valuation environments. Note that the current CAPE level is about 1.2 standard deviations above the 50-year average, though its historical significance is likely clouded by the dot-com bubble, which was a 4+ standard deviation event at peak, pulling up the average and standard deviation of the series (the 50-year average of the series was around 15 in 1995, but it currently approaches 20).

Similarly, a ratio like CAPE does not incorporate the new low interest rate and accommodative central bank paradigm. Skeptics argue that historically unprecedented interventionist policy from global central banks means valuation should be higher on a relative value basis when compared to the low yields available in the bond market. Surely there is merit to this argument with the Fed and ECB keeping rates low, and the Bank of Japan going so far as to purchase equity funds as part of its quantitative easing program. A consequence of these low-rate policies is, of course, to push investors into riskier asset classes, such as equities, in the search for an adequate portfolio return.

To paraphrase an old saying…nobody rings a bell at peak valuation. As you can see from the previous charts, the market has spent the overwhelming majority of the last 30 years in overvalued territory despite several significant drawdowns during that period. Not only that, but the market has shown the capability to push the multiple to much higher levels in the relatively recent past. Whether the market will experience a valuation-driven drawdown is unclear; the ratio is not necessarily signaling a crash, but lower forward returns in general. In fact, CAPE could potentially fall despite a steadily rising equity market if corporate earnings continue to grow, inflation remains tame, and the impact of the 2007-2009 crisis begins to fall out of the ratio’s denominator (which, as explained previously, uses 10-year inflation-adjusted earnings). Indeed, valuation metrics have little ability to predict short-term market returns. The correlation between longer-term returns and valuation, however, is undeniable, as is the level of risk with the level of valuation.

As we stated previously, valuation in and of itself is not a catalyst. Ultimately, the market will likely only re-rate lower in a significant way with the presence of a negative catalyst. Benjamin Graham’s value investing principles utilize valuation as a margin of safety: lower valuation equals higher margin of safety and vice versa. We think this applies to the market at large as well; negative catalysts are softened in lower valuation regimes, while higher valuation regimes exacerbate them. And, in the world we live in, where potential negative catalysts abound, we advocate a cautious, vigilant approach.-A.G.

Domestic stock indices continued this year’s strength in June, though hawkish signals from central bank figures caused a slight sell-off in the second half of the month. US large-cap stocks, as measured by the S&P 500 Index, gained 0.6% to bring year-to-date gains to 9.3%. US mid-cap stocks, as measured by the S&P 400 and the Russell 2000 small-cap index gained 1.6% and 3.5% for the month, respectively. International developed stocks, as measured by the MSCI EAFE Index, posted a small loss of -0.1%. The MSCI Emerging Markets Index, which has gained over 18% in the first half of the year, rallied 1.1% in June. At the sector level, financials led the way with a 6.4% return in June, as Congressional leaders signaled a continued interest in pursuing deregulation, particularly a restructuring of capital requirements under Dodd-Frank. In addition, the Federal Reserve announced in late June that, for the first time in seven years, all 34 of the country’s largest banks passed the annual stress test mandated under Dodd-Frank. This led the way for approval of the banks’ plans to return capital to shareholders via dividends or share buybacks. The technology sector, which has led the market higher to start the year, was a laggard in June, posting a -2.7% return for the month.

The S&P 500 traded up over 1.8% through June 19th before selling off 1.2% through the month-end after the US Federal Reserve raised interest rates and outlined plans to reduce the size of its balance sheet and European Central Bank (ECB) head Mario Draghi signaled optimism about inflation in the Eurozone. Market volatility, as measured by the CBOE Volatility Index (VIX) trended higher throughout the month, closing at 11.18 after opening the month at 10.41. The VIX, which remains well below long term averages, has received increased interest in recent months as investors pile into exchange-traded products that attempt to track the index. Though headline volatility remains benign, elevated levels of volatility are appearing in other areas of the market, most notably in technology stocks. The VXN, which tracks volatility of the NASDAQ 100 Index, rose 36% in June after a 12% rise in May, signaling rising investor fear in the technology sector.

Fixed income markets were generally weak in June, with the Bloomberg Barclays US Aggregate Index posting a -0.1% return for the month. Government bond interest rates generally rose in the US in Europe after hawkish comments from Fed and ECB officials. In the US, the 10-year Treasury yield rose 9 bps to close the month at 2.30%, though the 30-year yield closed the month 3 bps lower at 2.83%. The short-end of the curve rose sharply, with the 2-year Treasury yield rising from 1.28% to 1.38% in June. Mario Draghi’s comments were particularly impactful to government bonds in Europe, as the German and UK 10-year bond yield increased 16 bps and 21 bps to 0.46% and 1.26%, respectively, in June.

The S&P GSCI Total Return Index returned -1.9% in June, bringing year-to-date losses to 10.2%. The commodity complex continued to be weighed by falling energy prices. WTI crude oil opened the month at $48.63/bbl., and traded lower to $42.53/bbl. by June 21, before rallying sharply to close the month at $46.33/bbl. US drillers continue to increase production, Libya and Nigeria have increased production after war and terrorism related slowdowns, and OPEC struggles to find consensus on further production cuts. The precious metals sub-index also struggled to a -2.8% return in June as gold, which trended higher by over 7.7% to start the year, sold off in June to close the month at $1,241/oz.

The US dollar continued its slide against most major currencies in June, leading to a -1.4% return for the US Dollar Index, which measures the US dollar’s value against a basket of 6 foreign currencies. The only weaker currency was the Japanese yen, as Bank of Japan officials signaled a continued commitment to accommodative policy at its June meeting. After falling sharply in the wake of the US election, the Mexican peso has rallied over 13.8% against the US dollar in 2017, as the administration’s stance toward Mexico has softened in recent months.

We’re thankful for the continued interest and feedback. Please feel free to contact us with questions or comments.

Sincerely,

Arthur Grizzle & Charles Culver

Managing Partners

Martello Investments