According to legend, he was known amongst his peers for his sense of honor and his integrity in the pit. Though he died from lymphoma at 39 in 1991, there remains a 2-hour video lecture he gave to new floor traders in 1989 available here. I like to watch his lecture for a few reasons. First, it simply makes me feel better that whatever my trading-related headache for the day, I’m glad that I can do it from the relative comfort of a computer screen instead of how they did it back then. In Charlie D’s world, I would have had to call up the broker, scream at a guy through the phone, who would in turn have to scream at another guy to relay what I wanted to do, who would then have to scream at yet another guy to actually get the order done. Complaining about tabs versus spaces in our upload file or repeated pop ups seem like small problems when put in that context.

I know I’m a trading history nerd, but Charlie D’s lecture should be required listening for every trader and financial advisor because it is full of gems. Over 2 hours, he covers trading psychology: when to get out, how to take a loss, how to take a gain, and managing risk systematically. A few examples:

Most importantly, he discusses the value of having a puke point. A puke point is the mechanism that allows you to take your lumps in a losing trade and live to fight another day. From Charlie D:

“You’ve gotta have a puke point. When you’re long at 4, don’t look to buy ’em at 2…You want to get out! You want to throw those contracts up all over your shoes. That’s a puke point. The people that do the best in here are people that have a low puke point. When you have a position on that goes against you, you gotta get out.”

A puke point is about more than taking a loss in the purest trading sense. It speaks to the way a person processes information. We know from behavioral finance that most investors act irrationally handling gains and losses, opting to cut their gains early and let losses cascade. This has as much to do with banking profit or admitting defeat as it does with addressing how we process new information in a biased way. Our brains are naturally biased against disconfirmatory evidence, opting to place greater emphasis on information that agrees with our preconceived biases. This nasty cognitive defect, which social scientists attribute to our evolutionary need to trust each other, is a contributing factor to the best and the worst of us. Sure, it contributes to our inability to initially grasp when we are defrauded or betrayed, but it also allows us to form meaningful relationships. You win some, you lose some. Those with a low puke point run at the first sight of danger, while those with a high puke point require many shots of disconfirming evidence to change paths.

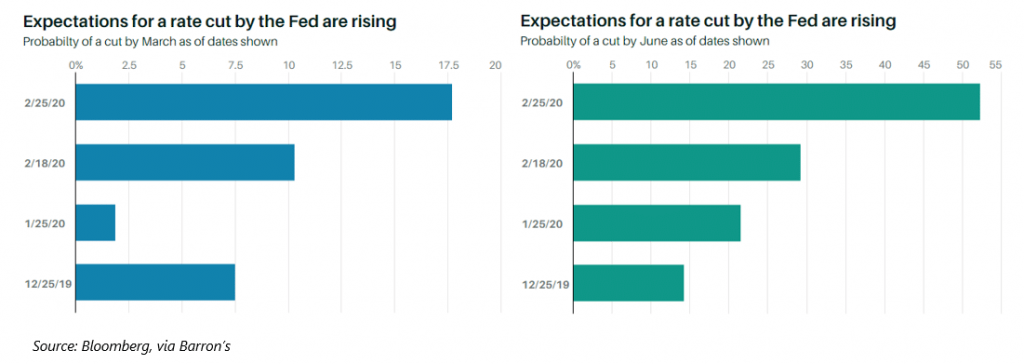

When we think about the evolution of the market over the last decade, we can only conclude that the market collectively has developed an unshakeable belief in the sustainability of rising prices. This is driven by several factors, not the least of which is the continued faith in the ability of the biggest sugar daddy of them all, the Federal Reserve, to step in and calm markets when called upon. This allows market participants to shake off bad news (an earnings recession in the United States, slowing growth, a weak and temporary resolution to a trade deal, and lately the potential global pandemic in the form of coronavirus) all the while marching to record highs. Some folks call this complacency; Charlie D would call it a high puke point, and he would be appalled to see it virtually everywhere.

The thing about complacency: it’s fine until it’s not. Everything appears normal until the exact moment you throw up all over your shoes. If you have kids, you know. The action over the last two days has laid bare what happens when a very tolerant market is awakened after many quarters of ignoring bad news. The last two days, each of which saw an S&P 500 return down more than 3%, is astronomical by the financial world’s standards. Let’s take a deeper look at that:

The long-run standard deviation of stock returns is roughly 1% daily. According to statistics, a down-three-standard-deviation event should occur approximately once every three years or so (1 in 741 days, or 0.135% of the time, based on 252 trading days in a year). The probability of two consecutive days like that is predicted to be once every 2,117 years (0.135% * 0.135% of the time). And this isn’t the first time we’ve seen these kinds of statistical oddities in the market. In fact, the market has been down three standard deviations for two consecutive days a total of 8 times in just the past twenty years. Unfortunately, the real conclusion here is that reality is a poor match for the theoretical statistical framework under which the entire financial industry operates, but that’s a great topic for another day.

It’s not as though the coronavirus, the headline cause for the increased volatility, appeared out of nowhere over the weekend and spooked the market. The seriousness of the virus has built for weeks while the market was missing its puke point! Only after an announcement of new disease clusters in Europe, South Korea, and Iran did the market even begin to price in the potential global deflationary impact of a pandemic. This will ultimately play out one of two ways. It could, like the swine flu hysteria or the most recent Ebola scare, peter out after a few months when global health authorities get it under control. Or, it could result in a more serious pandemic. It’s obviously impossible to know now. Personally, I believe in the ability of the medical community to find solutions. And the White House recently announced a $2.5 billion plan to combat the virus through additional funding for vaccines, treatments, and protective equipment.

Coronavirus aside, a clear-eyed view of the market leaves us with these sobering truths:

Will this lead to a more significant correction in stocks than the 6% or so that we’ve seen over the last two days? Who knows. Still, the stock market’s inability to price the risk of this virus incrementally should be troubling to all investors. We have seen these increasing risks reflected in the bond market over the last several months, with the US 30-year treasury yield falling to unprecedented levels, touching 1.8% yesterday. We feel strongly that the market reaction to this news is just the latest example of structural weakness that we have highlighted in many of our previous letters . Whether the texture of the next significant correction for equity markets will look more like 1937, 1987, or 2007 is a complete unknown, but given the seeming inability of the market to process negative information efficiently, we expect that we are in for more events like the last 2 days and the volatility blowup of February 2018, where equities fall sharply in very short periods of time. In such an environment, many traditional risk management metrics like momentum trading or moving averages are, as my grandmother used to say while dealing weak cards in nickel poker, “no apparent help.” Market shocks are necessarily against consensus, that’s what makes them shocks.

Yack.

Be safe out there.

Artie